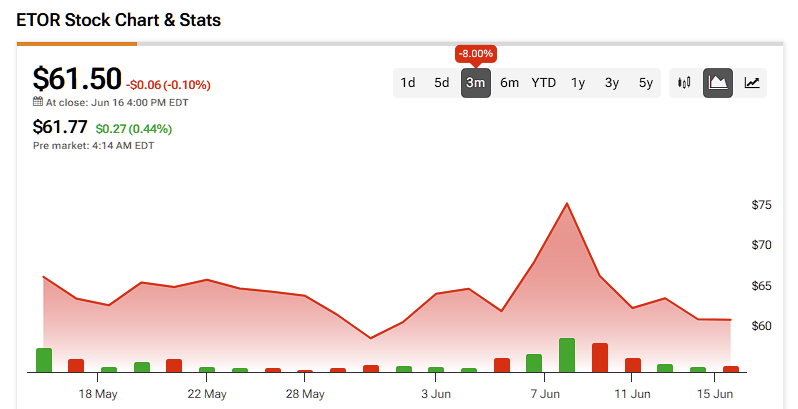

eToro (ETOR) is a primarily crypto-focused trading platform that debuted as a publicly traded company in May of this year, at approximately $70 per share, and has reached a peak of $75 per share earlier this month. The stock price has cooled since then, but the value proposition behind this hot new retail broker hasn’t.

This new entrant to the capital markets offers a distinct model compared to its competitors, aiming to provide a “social-first” trading platform where traders not only execute trades but also share their strategies and portfolios. This creates a persuasive value proposition and a clear competitive differentiator for eToro.

While most IPOs are priced for perfection—and that’s often when the trouble starts—eToro’s stock doesn’t look like a bargain, but it also doesn’t seem to be trading at stretched forward multiples. On the contrary, this gives me some reason for cautious optimism about its investment case.

Of course, eToro is still within its lock-up period, so investors can expect significant volatility in the short term. For that reason, I’m taking a speculative Buy stance on ETOR.

By mid-2025, crypto and online trading are far from niche, and the space is populated with major publicly traded players, including Coinbase (COIN) and Robinhood (HOOD). So, with eToro now entering the public markets, the question is what sets it apart from the rest.

The most straightforward answer is the platform’s unique social investing element. Like other trading platforms, eToro provides access to cryptocurrencies, ETFs, and other assets through a sleek and user-friendly interface. What really stands out is that users can follow other investors’ portfolios, view their performance, and even automatically copy their trades (a feature known as “copy trading”).

This creates a much more collaborative investing experience, allowing users to build diversified portfolios in one place, which is something that competitors like Robinhood are only starting to catch up with. Thanks to this social-first model, eToro has already established a global footprint with 3.6 million funded accounts, primarily in Europe and the United Kingdom, which gives it a competitive edge that is still difficult to replicate at scale.

Of course, with its strong focus on crypto trading, most of eToro’s revenue still comes from crypto-related activity. In the most recently reported quarter (1Q25), approximately 93% of total revenue came from cryptoassets, a slight decrease from 97% in 1Q24. That’s why it seems fairly apparent that eToro’s stock should move largely in sync with Bitcoin (BTC) and broader crypto market swings. In other words, it’s going to be a volatile ride.

The good news is that, for more risk-averse investors, despite only small steps toward diversifying revenue sources, eToro has been progressing relatively well, especially since top-line growth hasn’t suffered a significant decline. In 1Q25, revenue increased from $3.4 billion to $3.8 billion, a 11% year-over-year rise, driven in part by other segments, including equities, commodities, and currencies, which grew 32% during the same period.

However, the most encouraging sign is that eToro increased its number of funded accounts by 14% year-over-year. While its 3.6 million funded accounts are still only about one-seventh the size of Robinhood’s, eToro is growing at twice the pace, and this is a clear sign that the social-first model platform is gaining momentum in markets where it still has plenty of room to grow.

The caveat, though, is that in the latest quarter, eToro reported negative gross margins from its crypto business, down from 3.6% in 1Q24 to -0.8%, mainly due to an 11% increase in costs. Management attributed this to ramped-up marketing spend during a strong window of opportunity in the crypto market. While this kind of margin pressure isn’t unusual for growth-stage companies, it’s still too early to tell when (and especially if) eToro can eventually hit similar margin levels as Robinhood and Coinbase, both of which are now posting gross margins north of 85%.

Valuing recent IPOs is always tricky given their short public track record, but there are already a few takeaways from where eToro trades today. With 75.7 million shares outstanding and a stock price of $61.50, eToro’s market capitalization is approximately $4.65 billion. That puts the stock at about 5.2x book value—not much lower than Coinbase’s ~6x multiple, and well below Robinhood’s ~8x multiple.

If eToro’s book value may seem a bit stretched, on the earnings front, eToro trades at 24.6x estimated 2025 earnings. When you factor in expected EPS growth of around 14.4% CAGR over the next 3–5 years, that gives it a PEG ratio of roughly 1.7x—less than half of Robinhood’s 4.4x PEG and also way lower than Coinbase’s 2.7x multiple.

Of course, it’s still early, but the trend suggests that both Robinhood and Coinbase, which are further along in their business lifecycles, are likely to grow revenues at a slower pace. So while their valuation premiums might be justified to some degree, I would argue that eToro’s current multiples don’t look expensive—in fact, they seem a bit conservative.

Wall Street sentiment on ETOR skews slightly bullish, though some caution remains around the investment thesis. Of the 15 analysts covering the stock, eight rate it a Buy, while seven recommend holding. ETOR’s average price target is $74.78, implying a potential upside of approximately 21.5% from current levels.

Evaluating newly public companies can be challenging, as IPOs often come with heightened volatility while the market establishes a fair valuation and the company begins reporting financial results as a public entity. In eToro’s case, its performance remains closely tied to the crypto market, with the majority of its revenue derived from cryptoassets. Nevertheless, the platform has continued to grow its number of funded accounts—outpacing many peers—and appears well-positioned to maintain that momentum.

Given its early stage of profitability and relatively conservative growth assumptions, the stock does not appear overvalued. In fact, there may be meaningful long-term upside. That said, due to its reliance on crypto market dynamics and the inherent risks of emerging growth stories, I would currently categorize eToro as a speculative buy.